Step-by-step Guide to Pricing Your Product for Success in 2025

Have you ever wondered why some products flop, even when they seem perfect? Often, it comes down to pricing. If you want to price your product for success in 2025, you need a clear, step-by-step plan. Many businesses miss the mark by guessing or copying others, leading to costly mistakes. For example, Google Glass lost early adopters because its high price did not match what customers valued. When you price your product right, you avoid these pitfalls, stay competitive, and keep customers happy. You also make sure you follow rules like VAT, so you do not face surprises later.

Key Takeaways

Know all your costs. This means fixed and variable costs. Set a price that covers these costs. This helps you avoid losing money.

Check your market and competitors often. This helps you find the right price range. It also helps you stay competitive.

Learn what your customers value. Find out how much they will pay. This helps you set a fair and good price.

Pick a profit margin that fits your industry. Make sure it matches your business goals. This helps your business grow over time.

Use pricing strategies like cost-plus, value-based, or competitor-based. Choose the one that fits your product and market.

Balance the 3 C’s of pricing. These are cost, competitors, and customer value. This helps you find the best price.

Set a clear launch price. Tell people why your product is valuable. Be ready to test and change your prices if needed.

Watch your sales and the market all the time. Change your prices when needed. This keeps your business strong.

Costs

Getting your product price right starts with knowing your costs. If you skip this step, you might set a price that leaves you out of pocket. Let’s break down what you need to include.

Variable Costs

Variable costs change with how much you make or sell. If you produce more units, these costs go up. If you make fewer, they go down.

Materials

Materials are the items you need to create your product. This could be fabric for clothes, ingredients for food, or parts for gadgets. Always list every material and its cost. For example, if you bake cakes, flour, sugar, and eggs all count as materials.

Labour

Labour means the wages you pay people who help make your product. This includes your own time if you work on the product. If you hire someone to assemble, pack, or deliver, add their pay here.

Fixed Costs

Fixed costs stay the same no matter how many products you make. You pay these even if you sell nothing.

Rent

Rent covers the cost of your workspace. This could be a shop, a kitchen, or a small office. You pay this every month, so it’s a fixed cost.

Overheads

Overheads are other regular bills. Think about insurance, utilities, and advertising. These costs do not change with your sales volume.

Tip: Both direct costs (like materials and labour) and indirect costs (like packaging and overheads) must go into your pricing calculation.

Here’s a table to help you see the difference:

Cost Category | Description | Examples |

|---|---|---|

Fixed Costs | Stay the same each month | Rent, insurance, utilities |

Variable Costs | Change with production and sales | Materials, packaging, labour |

Total Cost per Unit

You need to know how much it costs to make one product. This is your cost per unit.

Formula

The formula is simple:

Cost per Unit = (Total Variable Costs + Total Fixed Costs) / Number of Units Produced

Example

Let’s say you make 500 candles in a month. Your materials and packaging cost £180. Your rent, insurance, and advertising add up to £1,170. Add these together (£180 + £1,170 = £1,350). Divide by 500. Your cost per candle is £2.70.

Note: Always include VAT or other taxes in your final price. If you forget, you might end up earning less than you planned.

You can use online product pricing calculators or tools like Siemens Teamcenter or aPriori Manufacturing Insights. These help you track every cost and avoid mistakes. Accurate costing means you set a price that covers your expenses and helps your business grow.

Market Research

You need to know what others charge before setting your price. Market research helps you find out where your product fits. You learn what customers want and how your competitors sell their products. Let’s look at this step by step.

Competitor Prices

Looking at competitor prices shows you the price range in the market. You should check both direct and indirect competitors.

Direct Competitors

Direct competitors sell products almost just like yours. If you sell handmade candles, other handmade candle brands are your direct competitors. You should:

Go to their websites and online shops.

Look at their prices, discounts, and bundles.

Read their product descriptions and reviews.

Use tools like Semrush or Similarweb to see their website visitors and marketing.

Try price monitoring software to get updates and alerts.

Tip: Real-time competitor price tracking helps you spot changes quickly. You can get alerts when a competitor changes their price.

Indirect Competitors

Indirect competitors sell different products that solve the same problem. For example, if you sell candles, wax melts or electric diffusers are indirect competitors. To research them:

Read what customers say in reviews and feedback.

Watch their social media for deals or new products.

Use tools like Ahrefs or LowFruits to see their keywords.

Ask your sales team or customers what other choices they look at.

You can also talk to vendors or people at trade shows. Sometimes, a short chat gives you more than hours online.

Market Position

After you know what others charge, see where your product fits. This is called price benchmarking.

Price Benchmarking

Price benchmarking means checking your prices against the market average. You want to know if your product is budget, mid-range, or premium. Online tools make this simple. Here are some popular ones:

Tool Name | Key Features | Pros | Cons |

|---|---|---|---|

SYMSON | AI-driven, price elasticity, simulations | Fast setup, smart features | Can lag with big updates |

Omnia Retail | Dynamic pricing, competitor monitoring | Good overview, less manual work | Complex algorithms, limited data |

PriceFX | Cloud-based, dynamic pricing, team collaboration | Easy to use, handles big catalogues | Needs partner support for changes |

PriSync | Price comparison, stock tracking | Tracks trends, bulk import/export | Setup can take time |

Competera | AI price optimisation, user-friendly | Reliable data, strong support | Limited forecasting |

You can also use apps like ShopSavvy or BuyVia for quick price checks and alerts.

Tools

Many tools help you track and compare prices. Some focus on online shops, others scan local stores. Here are a few you can try:

Shopzilla and Bizrate for wide product comparisons.

Camelcamelcamel for Amazon price history.

ShopMania and Yahoo! Shopping for price alerts and deals.

ShopSavvy for barcode scanning and price matching.

Note: AI-powered platforms like Klue and Crayon give you real-time data and help you spot trends before your competitors.

Market research is not something you do just once. Keep checking prices and trends. This way, you always know your place and can change your pricing to stay ahead.

Customer Value

Understanding what your customers value and how much they are willing to pay can make or break your pricing strategy. If you know what matters to your buyers, you can set a price that feels fair and attractive. Let’s look at how you can find out what your customers think and feel.

Willingness to Pay

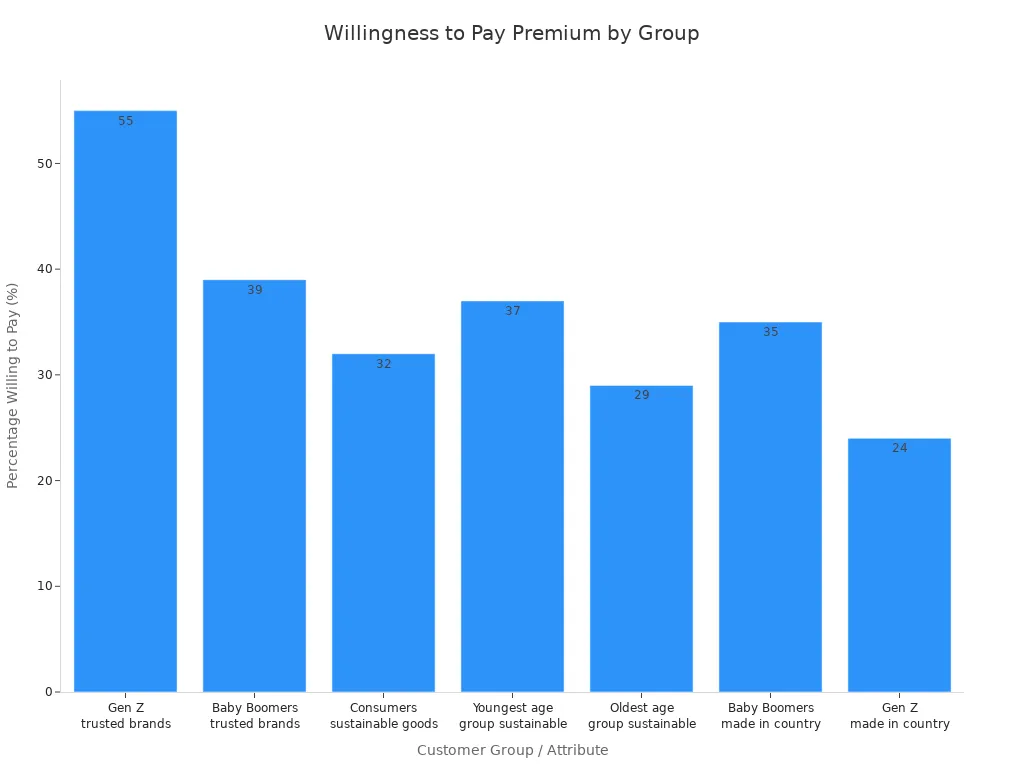

You want to know how much your customers are ready to spend. This helps you avoid setting your price too high or too low. Different groups of people have different ideas about value. Some care about trusted brands, others about where a product is made, or if it is sustainable.

Here’s a quick look at who is willing to pay more for added value:

Attribute / Demographic | Percentage Willing to Pay a Premium |

|---|---|

Gen Z consumers willing to pay extra for trusted brands | 55% |

Baby Boomers willing to pay extra for trusted brands | 39% |

Consumers willing to pay for sustainable goods | 32% (up from 24%) |

Youngest age group willing to pay for sustainable goods | 37% |

Oldest age group willing to pay for sustainable goods | 29% |

Baby Boomers willing to pay more for products made in their country | 35% |

Gen Z willing to pay more for products made in their country | 24% |

Surveys

Surveys are a great way to ask your customers about their willingness to pay. You can use simple questions or more advanced methods. For example, Conjoint Analysis shows people different product options and prices. This helps you see what features matter most. The Gabor-Granger technique asks if someone would buy at different prices. Both methods give you reliable data. Van Westendorp’s Price Sensitivity Meter helps you find the price range your customers accept. You can also use focus groups for deeper insights, but these work best with small groups.

Survey Method | Description | Reliability/Notes |

|---|---|---|

Conjoint Analysis | Shows product options with different features and prices. Measures trade-offs. | Highly reliable for detailed results. |

Gabor-Granger Technique | Asks if customers would buy at different prices. | Good for finding demand and best price. |

Van Westendorp's PSM | Finds the price range customers accept. | Useful for price range, less for exact price. |

Experimental Pricing | Tests prices in real or test markets. | Shows real buying behaviour. |

Tip: Make sure your survey is clear and your sample is big enough. This helps you get honest answers.

Feedback

Feedback from reviews, social media, and customer service chats gives you clues about what people value. Look for comments about price, quality, and features. Sometimes, a single review can show you what many customers think.

Perceived Value

Perceived value is what your customer thinks your product is worth. It is not just about cost. It is about how your product makes them feel and what problems it solves.

Unique Selling Points

Your unique selling points (USPs) set you apart. Maybe your product saves time, looks great, or uses eco-friendly materials. These features add value in your customer’s eyes. A strong brand or great design can make people pay more, even if the product does the same job as a cheaper one.

Value vs Price

People do not always buy the cheapest option. They buy what feels right for them. If your product offers something special, many customers will pay a bit more. Research shows that perceived value shapes both emotional and rational choices. Customers often pay more for products that match their lifestyle or give them a sense of status. Marketers use packaging, brand stories, and customer reviews to boost perceived value.

Perceived value shapes how much people want to pay.

Emotional appeal, brand trust, and good experiences all matter.

Customers justify higher prices if they feel your product meets or exceeds their needs.

Note: When you understand what your customers value, you can set a price that feels fair and keeps them coming back.

Profit Margin

Setting the right profit margin is a key step in pricing your product for success. You want to make sure your price covers all your costs and leaves enough room for profit. Let’s break down how you can choose a margin that works for your business and see how to use mark-up in real-world pricing.

Set Margin

Industry Standards

Every industry has its own typical profit margins. Knowing these standards helps you stay competitive and avoid pricing yourself out of the market. For example, in retail, gross profit margins in 2025 usually range from 30% to 50%. Net profit margins are lower, often between 2% and 10%. These numbers can change depending on your product type and business model. High-end or niche products often have higher margins, while products with lots of competition, like electronics, tend to have lower ones.

Here’s a quick look at common gross profit margins by product category:

Product Category | Gross Profit Margin Range | Key Margin Drivers |

|---|---|---|

Apparel & Accessories | Branding, seasonal pricing | |

Home Goods | 35-45% | Bulk buying, warehousing |

Consumer Electronics | 15-25% | High competition, price transparency |

Consumables (Subscription) | 55-65% | Subscription models outperform |

Tip: Keep your total inventory costs between 15% and 25% of your gross revenue. This helps you protect your net profit.

Business Goals

Your business goals also shape your profit margin. If you want to grow quickly, you might set a lower margin to attract more customers. If you aim for steady, long-term profit, you may choose a higher margin. Think about what you want to achieve:

Align your margin with your target profit and market position.

Focus on products that bring in the best margins.

Use pricing strategies like cost-plus or value-based pricing to match your goals.

Offer different pricing tiers to reach more customers.

Explain your value clearly so customers understand your price.

Keep an eye on your results and adjust your margin as needed.

Watch your competitors to make sure your margin stays strong.

Mark-up

Formula

Mark-up is the extra amount you add to your cost price to set your selling price. The basic formula looks like this:

Selling Price = Cost Price + (Cost Price × Mark-up %)

You can also work out the mark-up percentage with this formula:

Mark-up % = (Selling Price – Cost Price) / Cost Price × 100

Example

Let’s see how this works in real life. Imagine you sell a T-shirt that costs you £10. If you want a 50% mark-up, you multiply £10 by 0.5, which gives you £5. Add this to your cost, and your selling price is £15.

Here’s a table with more examples:

Industry | Cost Price | Mark-up % | Mark-up Amount | Selling Price |

|---|---|---|---|---|

Clothing Retail | £20 | 50% | £10 | £30 |

Food & Beverage | £10 | 100% | £10 | £20 |

Electronics | £500 | 30% | £150 | £650 |

Note: Mark-up is not the same as gross profit margin. Mark-up is based on your cost, while margin is based on your selling price. Mixing them up can lead to pricing mistakes.

Choosing a sustainable margin means you cover your costs, stay competitive, and reach your business goals. Keep checking your numbers and adjust as your market changes. This way, you build a healthy, profitable business.

Price Your Product

Setting the right price is more than just picking a number. You need a plan that matches your goals, your market, and what your customers want. In this section, you will learn how to price your product using proven strategies and the 3 C’s of pricing. Let’s break it down step by step.

Pricing Strategies

You have many ways to price your product. Each strategy works best in different situations. Here are some of the most effective methods for 2025:

Cost-plus

Cost-plus pricing is simple. You add a mark-up to your total cost to make sure you earn a profit. For example, if it costs you £10 to make a mug and you want a 50% mark-up, you sell it for £15. This method gives you predictable profits. However, it does not always keep you competitive if the market changes quickly.

Value-based

Value-based pricing focuses on what your customer thinks your product is worth. If your product solves a big problem or feels special, you can charge more. This approach often leads to higher profits and stronger customer loyalty. You need to know your customers well and understand what they value most. This strategy works best for unique or premium products.

Competitor-based

Competitor-based pricing means you look at what others charge for similar products. You then set your price to match, beat, or stay close to theirs. This keeps you competitive and helps you avoid pricing too high or too low. You must watch the market often because prices can change quickly.

Psychological

Psychological pricing uses tricks from human behaviour to make prices more appealing. Here are some popular techniques:

Charm pricing: Set prices just below a round number, like £4.99 instead of £5. This makes the price feel lower.

Remove currency symbols: Leaving out the £ sign can make spending feel easier.

Price anchoring: Show a higher-priced item first, so your main product looks like a better deal.

Bundle pricing: Offer products together at a lower combined price.

Scarcity and urgency: Use phrases like “limited time only” to encourage quick decisions.

These methods tap into how people think and feel about money. They can boost your sales and help you stand out.

Penetration

Penetration pricing means you start with a low price to attract customers fast. Once you build a loyal base, you can raise your prices. Big brands like Netflix used this strategy to grow quickly. This works well if you want to enter a crowded market or launch something new.

Tip: You can mix and match these strategies. For example, you might use cost-plus to set a base price, then adjust it with psychological tactics or competitor checks.

Here’s a quick list of other strategies you might see:

Price skimming: Start high, then lower your price over time.

Loss-leader pricing: Sell one item cheap to bring in customers who buy more.

Economy pricing: Keep prices low to attract budget shoppers.

Freemium pricing: Offer a free version, then charge for extras.

Bundle and optional product pricing: Sell products together or offer add-ons for extra profit.

Premium pricing: Set your price high to show quality and exclusivity.

3 C's of Pricing

When you price your product, you need to balance three key factors. These are called the 3 C’s: cost, competitors, and customer value. Let’s see how they work together.

Cost

Cost is your starting point. You must cover all your expenses, including materials, labour, rent, and overheads. If you price below your cost, you lose money. Use your cost as the lowest price you can accept.

Competitors

Competitors set the range for what customers expect to pay. If your price is much higher than theirs, you might lose sales. If it’s much lower, people may think your product is low quality. Check competitor prices often and adjust as needed.

Customer Value

Customer value is what your buyers think your product is worth. If they see more value, they will pay more. This is where your unique selling points and brand come in. Show your customers why your product is special, and you can charge a premium.

These three factors work together. For example, if your costs go up, you may need to raise your price. If a competitor drops their price, you might need to respond. If customers start valuing a new feature, you can adjust your price to match.

Note: The best price is not always the lowest or highest. It’s the one that balances your costs, matches the market, and fits what your customers value.

Here’s a table to help you compare the main pricing strategies:

Pricing Strategy | Profitability | Market Acceptance |

|---|---|---|

Cost-Plus Pricing | Predictable profit margins; may miss out on higher profits if demand is strong | Simple and stable; less flexible in fast-changing markets |

Value-Based Pricing | Often higher profits; works well for premium or unique products | Strong loyalty if value is clear; needs good research |

Competitor-Based | Keeps you competitive; risk of price wars if not careful | Good for crowded markets; needs regular monitoring |

Alternative Pricing Methods

Sometimes, you need other ways to price your product, especially if it’s new or innovative. Here are two popular methods:

Discounted Cash Flow (DCF): This method looks at the money your product will make in the future. It works well for new ideas with uncertain sales. You need to predict your cash flow and use a discount rate to find today’s value.

Market Comparison: This method checks what similar products sell for. It works best if you can find good matches. For new or unique products, this can be tricky.

Tip: For innovative products, DCF is often better because it handles uncertain sales and changing markets.

When you price your product, remember to review your strategy often. Markets change, and so do customer needs. Stay flexible, keep learning, and you will find the price that works best for your business.

Set and Test

Setting your product’s price is not the end of the journey. You need to launch with confidence, share your value, and keep testing to find what works best. Let’s walk through how you can set your launch price and adjust it for success.

Launch Price

You want your first price to grab attention and build trust. Here’s how you can do it:

Communication

When you launch, make your value clear. Highlight what makes your product different. Pick three or four key points that set you apart. Show how these features help your customers. Use simple language and focus on real outcomes, not just technical details. For example, if your product saves time or money, say so. Compare your offer to what customers already use. This helps them see why your product is better.

Tip: Tailor your message for each customer group. Use facts and numbers when you can. If you know your product lasts twice as long as a competitor’s, share that. Make sure your team knows how to talk about value, so everyone gives the same message.

Customer Expectations

Customers love a good deal at launch. You can use an introductory price to attract early buyers. Many people (about 80%) will try a new brand if they see a discount. Keep in mind, you might need to accept lower profits at first. Plan for this and make sure you have enough funds to cover costs. When you raise prices later, be ready for some customers to leave. Focus on showing real value, so people stay even when prices go up.

Here’s a simple launch pricing checklist:

Step | What to Do |

|---|---|

Research | Find out what your customers want |

Pre-launch | Test prices and see how people react |

Launch | Set your price, share your value, train your team |

Post-launch | Watch feedback and adjust if needed |

Test and Adjust

You can’t just set a price and forget it. Testing helps you find the sweet spot.

A/B Testing

A/B testing lets you try different prices with different groups. You might show one group a lower price and another group a higher one. Watch how each group reacts. This method uses real customer behaviour, not guesses. You can test things like price, billing options, or bundles. Always start with a clear idea of what you want to learn. Change one thing at a time, so you know what works. Make sure you have enough customers in each group to trust your results.

Try different price points or offers.

Test monthly versus yearly billing.

Experiment with bundles or special deals.

Note: Be fair and open. Avoid confusing or unfair pricing. This keeps your customers’ trust.

Sales Data

After launch, keep an eye on your numbers. Track sales, customer questions, and feedback. Look for patterns. Are people buying more at a certain price? Do you get more questions when you change your price? Use tools to help you spot trends. Work with your team to fix any problems fast. Keep testing and adjusting until you find the price that works best for you and your customers.

By setting, testing, and adjusting your price, you give your product the best chance to succeed.

Monitor and Adapt

You have set your price and launched your product. Now, you need to keep an eye on how things are going. The market never stands still. Your competitors change their prices. Customers change their minds. If you want to stay ahead, you must watch your numbers and be ready to act.

Track Metrics

You cannot improve what you do not measure. Tracking the right sales metrics helps you see if your pricing works. These numbers tell you if customers like your price or if you need to make changes.

Sales

Start by looking at your sales numbers. Do you see more sales after a price change? Are people buying bigger orders? You can use a few key metrics to get a clear picture:

Metric Name | Description | Why It Matters for Pricing |

|---|---|---|

Average Deal Size | Average money you make per sale | Shows if your price brings in bigger deals |

Conversion Rate | How many people buy after seeing your product | Tells you if your price attracts buyers |

Sales Cycle Length | Time it takes to close a sale | Reveals if your price speeds up decisions |

Sales Efficiency Ratio | Revenue per pound spent on sales | Checks if your price helps profits |

Revenue from Existing vs. New | Money from repeat vs. new customers | Shows if your price keeps customers loyal |

Percentage of Qualified Leads | Share of leads ready to buy | Tells you if your price attracts the right people |

Tip: Check these numbers every month. Patterns will show you what works and what does not.

Retention

Sales are great, but keeping customers is even better. If people come back to buy again, your price feels right to them. Watch your repeat purchase rate. If it drops, your price may be too high or your value is not clear. Loyal customers often spend more over time. They also tell others about your product.

Adjust Prices

You have tracked your numbers. Now, you need to know when to make a change. Price is not set in stone. Smart businesses adapt.

Market Changes

Markets move fast. Costs can rise. New trends appear. If your costs go up, you may need to raise your price. If a new trend makes your product more valuable, you can charge more. Always explain price changes to your customers. Show them the value they get.

Watch for new laws or taxes.

Look for changes in customer demand.

Check if your suppliers raise their prices.

Competitor Moves

Competitors can change the game overnight. If they drop their prices, you might lose sales. If they raise prices, you may have room to increase yours. Do not copy every move. Think about your value and your goals.

Note: Use competitor price tracking tools to get alerts. This helps you react quickly without guessing.

Stay flexible. Review your prices often. Small changes can make a big difference. When you monitor and adapt, you keep your business strong and ready for anything.

Promotions & Communication

Promotions and clear talking can make your pricing plan better. If you plan your offers well and talk about price changes, you keep customers happy and loyal. Let’s see how you can use promotions and honest talking to boost sales and build trust.

Promotions

You want your promotions to get attention and make people act. The best promotions in 2025 are short, focused, and easy to understand. They help you get new customers and keep your regular ones coming back.

Discounts

Discounts are a classic way to get more sales fast. You can give a percentage off, a set amount off, or a buy-one-get-one-free deal. These offers work best when they feel special or urgent. For example, a 24-hour flash sale can make people excited and want to buy now.

Discounts and coupons give customers instant value.

Flash sales and free samples make people act quickly.

Abandoned cart emails with special offers help bring back lost sales.

You can also use email marketing to send special discounts to your best customers. This makes them feel important and more likely to buy again. Many businesses get great results by giving discounts during holidays, product launches, or busy seasons.

Limited Offers

Limited offers make your product feel special. You might give early access to a new product or a special deal to the first 100 buyers. These promotions work because people do not want to miss out.

Use countdown timers on your website to show when an offer ends.

Try “while stocks last” deals to make people hurry.

Offer free shipping for a short time to get bigger orders.

Other good ideas include pay-per-click ads to reach new buyers and making your website easy to find deals. Sending personal messages and giving great service also helps people come back.

Tip: Always check how well your promotions work. Track sales, redemption rates, and customer feedback to see what works best.

Communicate Changes

When you change your prices, how you tell people is just as important as the change. Honest, open talking keeps your customers on your side.

Transparency

Customers want to know why prices go up or down. If you explain your reasons clearly, most people will understand. Studies show that 94% of shoppers stay loyal to brands that are open about pricing. Brands like Warby Parker and Everlane have grown by sharing cost breakdowns and explaining price changes. When you hide fees or make sudden changes without warning, you risk losing trust. In fact, many people leave if they see surprise charges at checkout.

Tell customers about price changes before they happen.

Explain the reasons, like higher material costs or better quality.

Use simple, honest words.

Customer Trust

Trust is the base of any good business. When you talk openly, you show customers you respect them. This builds loyalty and keeps people coming back, even if prices go up. If you need to raise prices, link the change to something good, like better service or eco-friendly materials. Brands that do this well, like Patagonia, keep their customers even when times are hard.

Note: Clear, caring talking about price changes can help keep more customers by up to 15%. Always put your customers first when you share news about pricing.

By planning smart promotions and being open about price changes, you build loyal customers who support your business for a long time.

You now have a clear path to Price Your Product for success. Remember, regular reviews help you stay agile and protect your margins. When you adapt your pricing, you build trust and keep customers loyal. Try using tools like surveys, A/B testing, and market research platforms to track what works.

Stay flexible with pricing models and review your strategy often.

Use analytics to spot trends and make smart changes.

Ready to take action? Start today and watch your business grow!

FAQ

How often should you review your product prices?

You should check your prices at least every quarter. If your costs or the market change quickly, review them more often. Regular checks help you stay competitive and protect your profits.

What if your competitors lower their prices?

Stay calm. Look at your value and what makes you different. You do not always need to match their price. Sometimes, you can offer better service or unique features instead.

Should you include VAT in your displayed prices?

Yes, you should show VAT in your prices if you sell to the public. This keeps things clear for your customers and helps you follow the law.

How do you know if your price is too high?

Watch your sales and listen to feedback. If customers stop buying or complain about price, you might need to adjust. Try small changes and see how people react.

Can you change your prices after launch?

Absolutely! You can test new prices any time. Use A/B testing or special offers to see what works best. Just make sure you explain any changes to your customers.

What is the best pricing strategy for new products?

Start with market research. Try a launch offer or penetration pricing to attract buyers. Watch your results and adjust as you learn more about your customers.

How do you handle price objections from customers?

Listen first. Explain the value and benefits of your product. Sometimes, you can offer a small discount or bundle to help close the sale.

Tip: Always stay honest and open when talking about price. Customers trust you more when you explain your reasons.

TangBuy: A Smarter Way to Dropship in 2025

If you're looking to stay competitive with dropshipping in 2025, speed and trend-awareness are key. TangBuy helps you stay ahead with real-time product trends, fast fulfilment, and factory-direct sourcing. With over 1 million ready-to-ship items, 24-hour order processing, and seamless Shopify integration, TangBuy makes it easier to test, scale, and succeed in today's fast-moving eCommerce landscape.

See Also

How To Successfully Start A Dropshipping Venture In 2025

Complete Instructions For Selling Wholesale Through Online Platforms 2025

Detailed Approach To Maximising Profits Selling On eBay In 2025

The Ultimate Handbook For Profitable eBay Sales In 2025

Top 25 Affordable Products To Increase Store Profits In 2025